Are Certificate Of Deposits (CDs) Safe?

In the world of personal finance, finding ways to make your money work for you while keeping it safe is paramount. One often-overlooked option that deserves attention is the Certificate of Deposit (CD). In this article, we’ll delve into what CDs are, how they work, and why they can be a valuable addition to your financial portfolio.

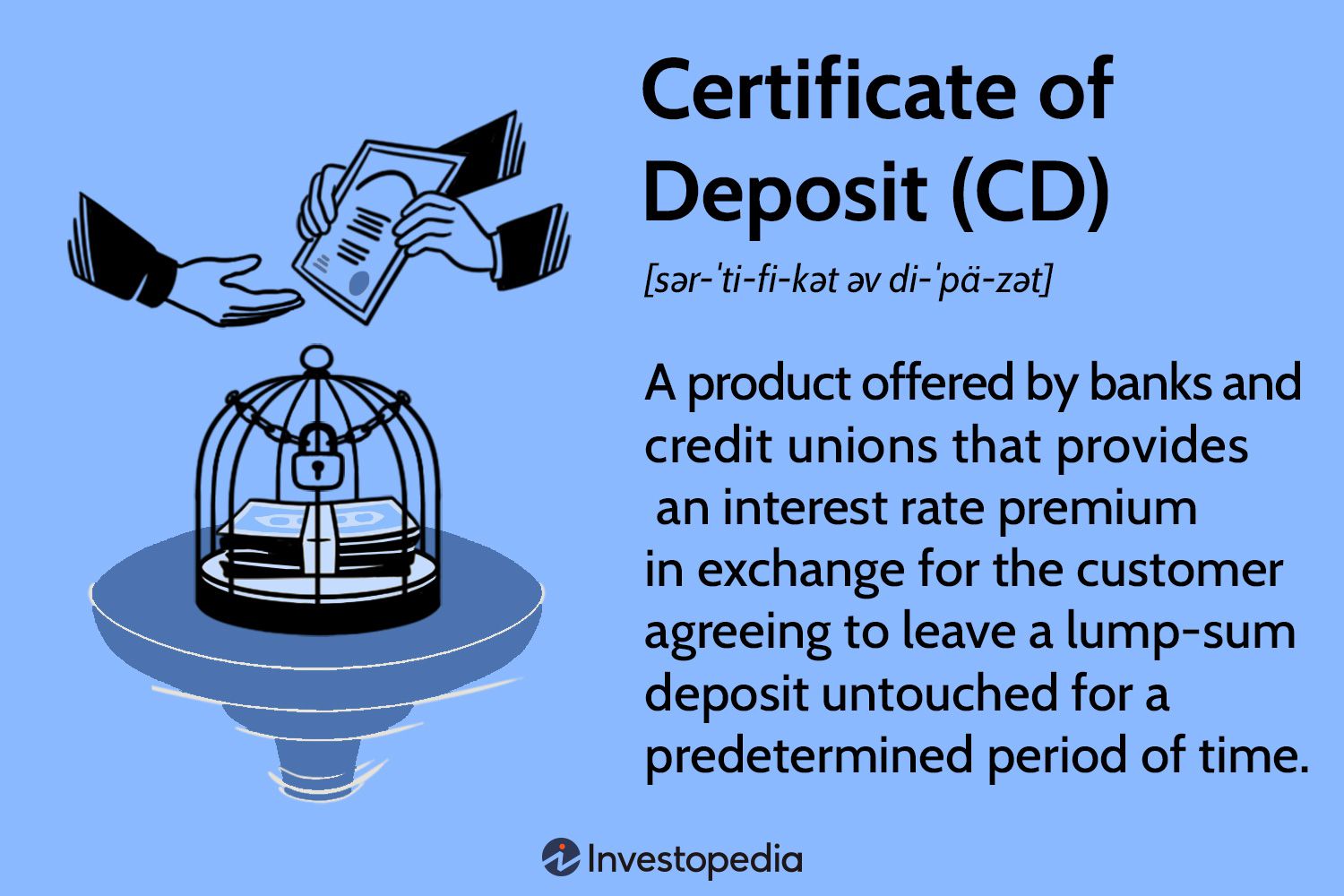

What Is a Certificate of Deposit(CD)?

A Certificate of Deposit, commonly referred to as a CD, is a type of savings account offered by banks and credit unions. Unlike a regular savings account, CDs typically offer higher interest rates in exchange for locking your money away for a set period of time, known as the term or maturity period.

How CDs Work

Opening a CD account is similar to opening a savings account in that there may be a minimum initial deposit you’re required to make. You’ll also have to choose a CD term, which is the length of time you agree to keep your money tied up in the CD.

CD terms can range from as little as 28 or 30 days up to 10 years or more, depending on the bank or credit union. As a general rule of thumb, the longer the CD term, the higher the interest rate you can earn. Some banks may, however, offer promotional CDs that feature higher rates with shorter terms.

The annual percentage yield (APY) for CDs is typically fixed, meaning you earn the same rate for the entire CD term. However, there can be exceptions. Bump-up and step-up CDs, for example, offer the opportunity to raise your rate once or twice during the CD term.

Once a CD matures, you’re free to withdraw the money you saved, along with interest earned. However, it’s important to note that many banks automatically roll your savings into a new CD at the end of the term if you don’t specify that you want to make a withdrawal.

Pros of Using a Certificate of Deposit for Savings

There are several reasons why you may consider using a CD for managing your savings goals. Here are some of the main benefits or advantages of saving money with certificate of deposit accounts.

1. Safety

Along with savings accounts and money market accounts, CDs are some of the safest places to keep your money. That’s because money held in a CD is insured.

So long as you purchase your CD account through an FDIC-insured bank, you’re covered in case the bank shuts down or goes out of business. The current coverage limit is $250,000 per depositor, for each account ownership category, per financial institution. At federal credit unions and the majority of state-chartered credit unions, the NCUA insures your money up to the same limits.

2. Guaranteed Returns

CD accounts offer predictability in that it’s relatively easy to determine how much interest you’ll earn over time, since rates are typically fixed for the entire term. Certificate of deposit calculators allow you to plug in the amount you’re saving and your APY to gauge how much your money will grow.

For example, say you open a five-year CD with $5,000 and earn a 1.00% APY. At the end of your CD term, you’d have $5,255 and change. If you’re saving for a long-term goal that has a specific end date, you can tailor your choice of CD terms and interest rates to help you meet your goal.

3. Higher Rates

Compared to savings accounts or money market accounts, CDs potentially can offer higher interest rates on deposits. That’s because you agree to keep your money in the CD for a set time period. The interest rate and APY you earn depends on the bank, the CD term and the current interest rate environment.

When comparing high-yield savings accounts and CDs side-by-side, it’s helpful to see how interest rates compare. And if you’re opening a CD when rates are relatively low overall, you may lean toward a bump-up or step-up CD that allows you to capitalize when rates begin to rise.

4. No Monthly Maintenance Fees

With savings accounts or money market accounts, you may get charged a monthly maintenance fee to use the account, which can quickly eat into your interest earnings. Certificate of deposit accounts, on the other hand, typically don’t charge a monthly maintenance fee.

This means you get to keep all the interest you earn. Assuming you don’t need to withdraw money from a CD before it matures, CDs can be a fee-friendly way to grow savings.

Cons of Using a Certificate of Deposit for Savings

While CDs can be used to save for various financial goals, they aren’t always ideal for every situation. Here are some of the key downsides to know before opening CDs to save money.

1. Accessibility

With a savings account or money market account, you’re allowed to make a certain number of withdrawals of cash or transfer funds to a linked checking account. Certificate of deposit accounts, on the other hand, typically require you to keep the money in place until the CD matures. This means a CD likely isn’t the best choice for your emergency fund.

Savings accounts and money market accounts may also come with a debit card or ATM card. In the case of a money market account, you may also be able to write checks against your balance. Certificates of deposit typically don’t offer those features.

2. Early Withdrawal Penalties

CDs are designed for holding money that you don’t plan to spend right away. While you aren’t barred from taking money out of a certificate of deposit early, there’s usually a price to pay for doing so.

Banks and credit unions often charge an early withdrawal penalty for taking funds from a CD ahead of its maturity date. This penalty can be a flat fee or a percentage of the interest earned. In some cases, it could even be all the interest earned, negating your efforts to use a CD for savings.

3. Interest Rate Risk

Using CDs as a savings tool means being aware of what’s happening with interest rates. When rates are high, your CDs will generally yield a better return. But when rates are low, money held in CDs won’t grow as much.

CDs carry interest rate risk in that it’s possible to lock in savings at one rate, only to see rates climb. Unless you have a step-up or bump-up CD, you wouldn’t be able to take advantage of that higher rate without opening a new certificate of deposit.

4. Inflation Risk

Inflation means how prices for goods and services change over time. If inflation is rising, it could outpace the rate of return you’re earning on your CDs, especially in a low interest rate environment.

This means even though your savings is growing, it won’t stretch as far when it’s time to spend it. Notably, this is also a risk when keeping money in savings and money market accounts.

5. Lower Returns

Generally, the safer an investment or savings vehicle, the lower the rate of return. While CDs can offer stable returns and security, you may see your money grow faster by investing it in stocks or mutual funds.

Investing money in the market instead of saving in CDs could help you keep pace with inflation while enjoying higher returns. But keep in mind that there are risks involved with that as well.

(0 rating, 0 votes, rated)

(0 rating, 0 votes, rated)You need to be a registered member to rate this.